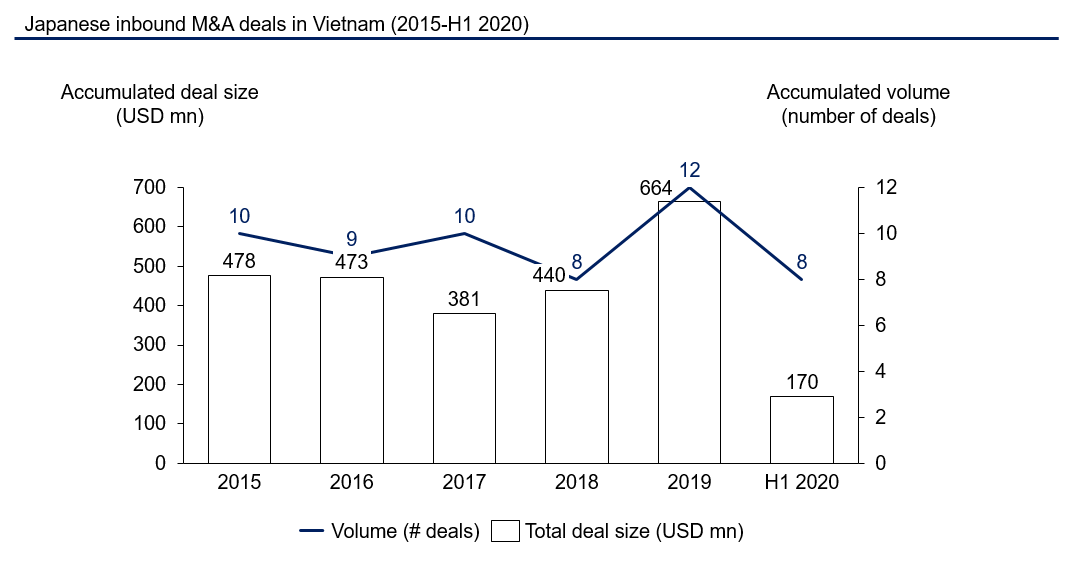

Since the country began opening up its economy in the late 1980s, Vietnam has been an attractive destination for foreign investors. In 2019, data from the Foreign Investment Agency (FIA) shows that Foreign Direct Investment (FDI) reached USD38.2 bn an increase of 7.2% compared to the same period in 2018. Japan has been highly active in the field of M&A as illustrated in the chart -below. In 2019, total Japanese inbound M&A deals amounted to more than USD 450mn in Vietnam with 12 deals*. During the same year, Japan was the 3rd largest contributor of foreign M&A deals in Vietnam in terms of deal value after South Korea and Singapore.

Source: Mergermarket, IGPI analysis * For disclosed deal value to be greater than or equal to USD 5 mn and / or the target’s turnover/revenue is greater than or equal to USD 10 mn

Financial services, agriculture, consumer among the key sectors of investments by Japanese firms

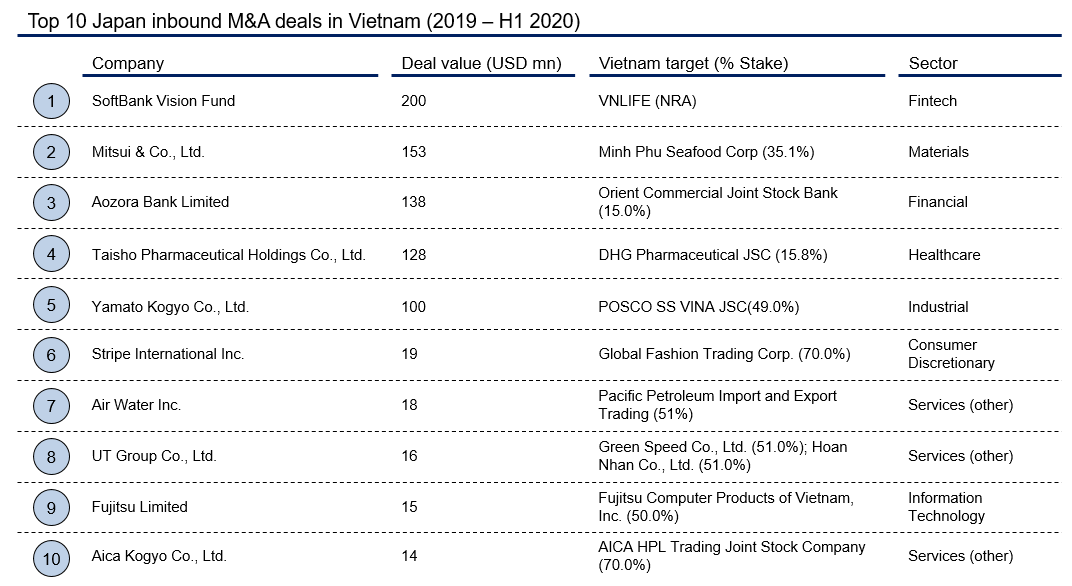

Historically, Japanese investors have been focusing on Vietnam’s rapidly growing financialservices sector. One of the notable transactions took place in December 2012 where Tokyo Mitsubishi UFJ purchased a 20% stake in Vietinbank for USD 743 mn. Local financial institutions are looking for strategic foreign investors to improve their business performance and to strengthen their balance sheet through capital injections. Recently in January 2020, Vietnamese mid-sized bank, Orient Commercial Joint Stock Bank (OCB Bank) divested 15% stake to Japanese Aozora Bank for USD 138 mn and the transaction currently represents the second largest deal in Vietnam by Japanese companies over the period 2019 – H1 2020 as shown in the table here-below:

Source: Mergermarket, IGPI analysis *For disclosed deal value to be greater than or equal to USD 5 mn and / or the target’s turnover/revenue is greater than or equal to USD 10 mn

Agriculture is also another driving force behind acquisitions as agricultural companies are looking to expand their technical capabilities. As the demand for increased productivity rises, the players in agriculture sector are looking into adopting technologies (i.e. agriculture technology or “Aggrotech”) to improve yield, efficiency, and profitability. In May 2019, Mitsui acquired a 35.1% stake in Minh Phu Seafood, a Vietnamese shrimp producer and processor for USD 153 mn and is the largest transaction by Japanese companies in Vietnam over 2019-H1 2020. According to Mitsui, this transaction will enable Minh Phu to achieve further growth through the application of digital technology including AI in farming ponds and processing plants and the enhancement of the efficiency in shrimp supply chain from farming to marketing. Additionally, manufacturing is another area of interest for Japanese investors since Japanese companies have higher technological capabilities in comparison to their Vietnamese counterparts and want to bring their expertise to the local companies to expand. Especially, during the current COVID-19 situation, many Japanese consumer and industrial goods manufacturers are considering to shifting their manufacturing bases from China to Vietnam in order to take advantage of more affordable labour costs here in Vietnam. Notably, Hoya Corporation, which manufactures hard-drive components, is expected to move from China to both Vietnam and Laos. Lastly, a large number of workers in Vietnam speak Japanese, which is a distinct advantage compared to other countries in the ASEAN region. On this matter, it is also important to highlight that around 300,000 Vietnamese people live and work in Japan, proving further benefits for both countries.ICT and digital transformation development

The information and communications technology (ICT) services is a fast-growing sector in Vietnam and will provide further foundation for the digital development of the country. In 2018, the country had an estimated 30,000 businesses across IT hardware, software, digital content and ICT services1. Vietnam benefits from a flourishing community of software developers and start-ups and developing digital products and services, attracting Japanese firms but also global attention as a significant regional hub. Though the digital transformation of Vietnamese firms is taking place slowly, the Vietnam government, large corporates and small-medium enterprises are playing the active roles of adopting and implementing digital transformation initiatives across their organizations. For example, FPT the leading ICT company in Vietnam, has set as one of its mission to be a pioneer in digital transformation to transform the country’s economy and society. On this aspect, in September 2020, IGPI and FPT Japan will jointly hold a webinar to provide insights on how corporates can design its digital transformation through corporate transformation in the Southeast Asian region. 1. Source: Vietnam Information Technology Outsourcing Alliance. 2018. Why Vietnam? Challenges in investing in Vietnam

The long-term outlook for further M&A activity by Japanese investors remains highly positive as Japanese firms continue to look outward and see Vietnam as an important and stable investment location that is growing. Vietnam has been a strategic market for Japanese companies investing overseas due to its close geographic proximity, low labour costs, large work force, its openness to investment by Japanese companies and the positive relationship that exists between the two countries. Furthermore, Vietnam targets to become the leading digital country and economy in the ASEAN region by 2030. Under the national e-commerce development master plan in 2021-25 and the national digital transformation programme to 2025, digital transformation represents a vital process to increase the competitiveness of the economy, while further developing the domestic market and increasing exports. Altogether, this will impact positively and transform multiple key sectors from manufacturing and agriculture to trade, payment, transportation, finance, healthcare and education. However, there are challenges to consider when foreign companies are investing and doing business in Vietnam. As with many developing economies, Vietnam is experiencing the rise of its cost of labor year by year. Therefore, it is necessary for Vietnam to create other advantages for itself. Another key challenge faced by foreign investors when acquiring Vietnamese companies is the lack of reliable and publicly available information on target companies. When conducting due diligence on a company in Vietnam, foreign investors often have to heavily rely on the documents and information provided by the target company and some private companies may also lack adequate financial reporting standards which provide further challenges for foreign investors. Finally, given the country still enjoys a strong economic growth compared to other ASEAN countries, foreign investors have to negotiate with high premium valuation of target companies particularly in fast growing sectors such as consumer, healthcare, retail, etc. Government support for M&A and other areas of investment opportunities

Despite the existence of these difficulties, we believe that M&A is still one of the most effective and rapid ways by which Japanese companies can gain access to the attractive Vietnamese market. Japanese companies are likely to continue to be one of the key countries leading the M&A investments in Vietnam. Moreover, the Vietnamese government has also streamlined the M&A process to encourage foreign investment. One the key initiatives is the upcoming equitisation process of state-owned enterprises. This represents great opportunities for foreign investors including Japanese firms to acquire a stake in large state-owned enterprises (SOE). Some examples of SOE include Vinacomin, VNPT, VinaPhone, MobiFone, VTV Cab, Thang Long Tobacco Company, Vinafood 1 and 2, Vinacafe, Vietnam Rubber Group, and Vietnam Chemical Group. In addition to SOE, the Deputy Prime Minister, Vuong Dinh Hue, has recently mapped out core fields for restructuring, all of which are to welcome capital injections from investors from Vietnam and abroad. These areas include finance and banking, public debts, and streamlining nonmanufacturing units, which will provide further business and investment opportunities for Japanese investors in the country. How can we help? IGPI Vietnam

IGPI Vietnam was established in 2016 to support the Vietnam government in the business revitalization of state-owned companies and disposal of non-performing loans of financial institutions. Through these projects, IGPI Vietnam supported the Vietnam government in reaching the ultimate goal of transforming and improving the quality and competitiveness of Vietnam economy. Today, IGPI Vietnam focuses on management consulting and M&A advisory supporting Japanese investors and local enterprises to expand their business and to find the best partners across sectors. We also act as a bridge between Japan and Vietnam and advise on a wide range of areas that include market entry strategy, potential target search, valuation, due diligence, M&A process management, post-merger integration. Our consultants are also able to speak both Vietnamese and Japanese languages fluently to assist our clients in their projects. About the Author

Kim-Lân Dang is Vietnamese born in France and is a Senior Manager at IGPI Singapore. He started his career in 2008 with PricewaterhouseCoopers Luxembourg and later joined in 2012 Ernst & Young Singapore. Before joining IGPI, he worked at BDA Partners and TC Capital in Singapore. Kim-Lân has vast experience in advising blue-chip private equity funds, entrepreneurs, and corporates on divestments and capital raises. He has executed M&A transactions across Vietnam and the rest of Southeast Asia covering various industries including consumer/retail, IT, telecommunications, financial services, and financial technologies.About IGPI

Industrial Growth Platform Inc. (IGPI) is a premier Japanese business advisory firm with presence and coverage across Asian markets. IGPI was established by former members of Industrial Revitalization Corporation of Japan (IRCJ) in 2007. IRCJ, a USD 100 bn Japanese sovereign wealth fund, is known as one of the most successful turn-around fund supported by the Japanese government. In 2017, IGPI collaborated with Japan Bank for International Cooperation (JBIC) to form JBIC IG, providing investment advisory services and supporting overseas investment. In 2019, JBIC along with BaltCap has jointly established Nordic Ninja, a EUR 100 mn venture capital fund to focus on deep tech sectors such as autonomous mobility, digital health, AR/VR/MR, artificial intelligence, robotics and IoT in the Nordic and Baltic region. In 2019, IGPI established IGPI Technology to focus in the area of science and technology. The company invests in technological ventures and provides hands-on management support. The company also provides business development support towards commercialization and monetization of technologies. Get in touch with us on strategic planning, market assessment and M&A related topics! IGPI Vietnam and Singapore – contacts:

This material is intended merely for reference purposes based on our experience and is not intended to be comprehensive and does not constitute as a digital transformation advice. Information contained in this material has been obtained from sources believed to be reliable, but IGPI does not represent or warrant the quality, completeness and accuracy of such information. All rights reserved by IGPI.

Kohki Sakata Chief Executive Officer

+65 81682503 k.sakata@igpi.co.jp

Kohki Sakata Chief Executive Officer

+65 81682503 k.sakata@igpi.co.jp Kim-Lân Dang Senior Manager

+65 91000273 k.dang@igpi.co.jp

Kim-Lân Dang Senior Manager

+65 91000273 k.dang@igpi.co.jp