Alongside the sale and purchase of expensive residential properties, the sale and purchase of coffee shops (A coffee shop is a collection of small-scale eating and drinking establishments that are an essential part of the local daily lives) have received prominent media coverage in Singapore. In June 2022, two suburban coffee shops were sold for approximately S$41.6 million (JPY4 billion) and S$40 million (JPY3.9 billion) respectively. They are comparable to a busy ground-floor shop in a prime downtown location. This article examines the background of coffee shops’ high value in Singapore, their role in daily life, and how they can increase their profitability and explores potential business opportunities for Japanese companies.

Highly priced and rare coffee shops: Only 400 coffee shops can be transacted

Singapore is a country with a small land area but active property investments with daily transaction reports rising. Examples of typical transaction reports: 1) In July 2022, the CEO of Three Arrows Capital, a virtual currency hedge fund that filed for Chapter 11 bankruptcy protection in the US, to sell a luxury bungalow (GCB) he had just purchased for S$48.8 million (approximately JPY4.7 billion). 2) In July 2021, the family of Grab’s (A super app platform) CEO, and the CEO of Secret Labs (manufacturer of gaming chairs) bought a GCB for S$40 million (approximately JPY 3.9 billion) and S$36 million (approximately JPY 3.5 billion) respectively. 3) In October 2020, it was also reported that the founder of British home appliance giant Dyson sold his penthouse, which he had purchased a year earlier for S$74 million (approximately JPY7.2 billion), for S$62 million (approximately JPY 6 billion). These expensive housing transactions are not limited to a few wealthy people. In HDB, where 80% of the population lives, the transaction price of resale properties is also at an all-time high, with a series of cases reported where properties were sold for more than S$1 million (approximately JPY 97 million).

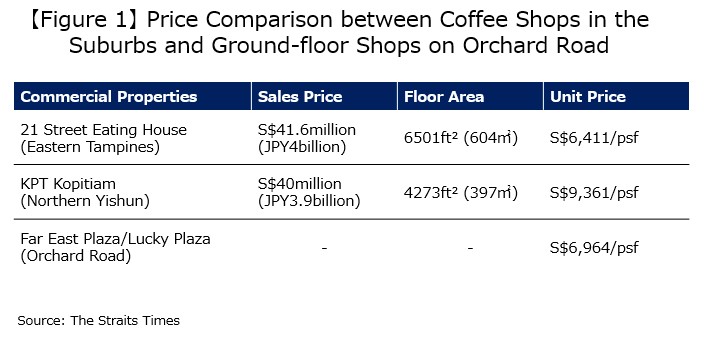

Alongside housing, the sale and purchase of coffee shops are increasingly reported in the press. Coffee shops are a collection of several small-scale eating and drinking establishments located usually on the ground floors of the busy town centre, HDB, and industrial estates. Many of which are owned by private companies and individuals, in contrast to “Hawker Centres” which are owned by the National Environment Agency (NEA). In June 2022, the news of the Eastern 21 Street Eating House in Tampines being sold for S$41.6 million (approximately JPY 4 billion) and KPT Kopitiam in Yishun in the north for S$40 million (approximately JPY 3.9 billion) hit the headlines. More surprisingly, both coffee shops were sold at a new historical high price. The Tampines coffee shop was purchased from the Housing and Development Board (HDB) for S$3.45 million (approximately JPY 330 million) in 1992, and 30 years later, it was sold for 12x the price, while the Yishun coffee shop was purchased for S$6 million (approximately JPY 580 million) in 2007 for 15 years after it was sold for nearly 7x the price. It is also astonishing to note that the acquisitions are leasehold (fixed term usage) and not freehold (unlimited term usage) and that the selling prices are comparable to a ground-floor shop in a prime location on Orchard Road, Singapore’s busiest shopping street (Figure 1).

Why are suburban coffee shops trading at such high prices? We believe there are two main reasons. The first reason is the limited number of outlets available for trading in the first place. There are about 2,200 coffee shops and similar eateries in Singapore, and about 770, equivalent to one-third, are set up by HDB on the ground floors of HDBs out of which 400 of these are sold to private companies and individuals in the early 1990s. In 1998, NEA has stopped selling them and switched to renting the owned coffee shops to private companies and individuals. In other words, only 400 coffee shops that are set up in public housing can be transacted. The second reason is that the coffee shops in Tampines and Yishun, which were sold at a historical high price, are large and scarce. The two coffee shops have 18 and 14 stalls of small-scale restaurant space, respectively, and are expected to attract a more significant number of customers as they can develop a wider variety of restaurants than many coffee shops, which typically have less than 10 plots.

However, the sale and purchase of coffee shops at high prices risk becoming a social problem in the form of increased rents borne by the tenants, small restaurants, which subsequently are passed on to consumers through increased food prices resulting in a larger burden on the household budget for consumers. In this context, National Development Minister Desmond Lee, in his parliamentary reply in July 2022, emphasised that an average of 15 coffee shop transactions in public housing have occurred every year since 2010, but that 70% of these transactions are for less than S$10 million (approximately JPY 970 million), with limited impact on household finances.

Coffee shops are like a ‘second kitchen’: Coffee shops perform well in the COVID-19 pandemic

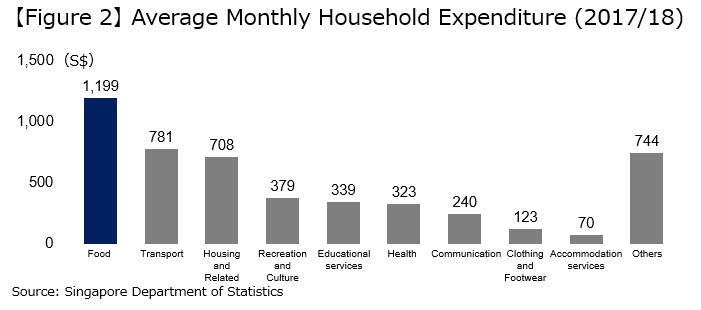

Singapore is often called the “Nation filled with food critics”. This article examines the critical role of food and drink and coffee shops in their socio-economic activities. The most recent household survey conducted by the Singapore government shows that the average monthly household expenditure on food is S$1,199 (approximately JPY 116,000), the largest of all categories (Figure 2).

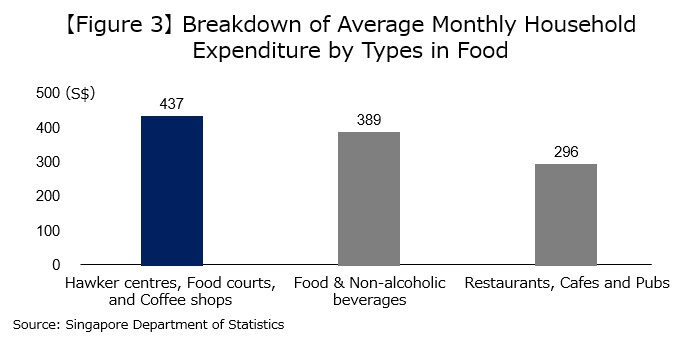

Looking further at food by detailed category, it can be seen that the average monthly household expenditure of S$437(approximately JPY 42,000) per month on categories in addition to coffee shops, including hawker centres and food courts is higher than food and non-alcoholic beverages (S$389) and restaurants, cafés and pubs (S$296) (Figure 3).

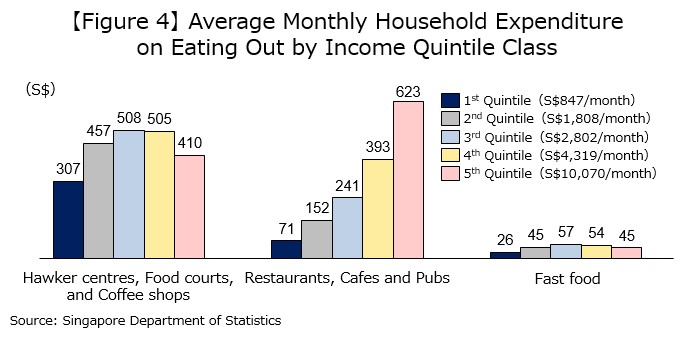

The fact that more was spent on coffee shops and hawker centres than on food and non-alcoholic beverages suggests that eating out or taking food away from home is more common in Singaporeans’ lives than cooking for themselves. Furthermore, looking at average monthly household expenditure by income quintile in the three food service categories, including fast food, it shows that the largest expenditure is on coffee shops and hawker centres, except for the highest income quintile with an average monthly household income of S$10,070 (approximately JPY980,000) (Figure 4). It is often believed that the main customers of coffee shops and hawker centres are low-income households, but in reality, coffee shops and hawker centres are almost like a ‘second kitchen’ for many Singaporeans, who use them daily.

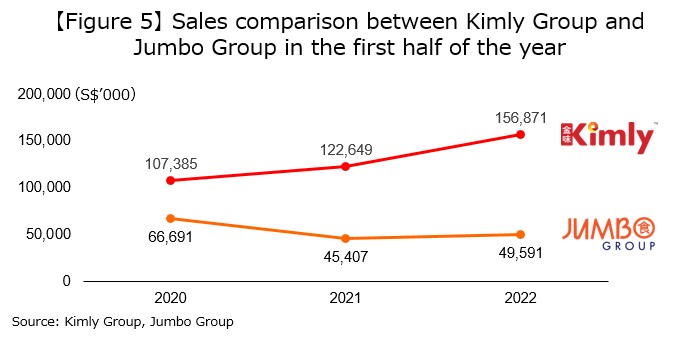

These food and beverage purchasing behaviours by Singaporeans will continue to grow as a result of new behaviours stemming from the outbreak of COVID-19, namely the increasing use of coffee shops adjacent to suburban HDB rather than restaurants in office blocks due to the spread of work-from-home. In fact, 30 new coffee shops are expected to be built in council housing over the next four years. A comparison of the performance of typical food service companies in COVID-19 also provides a glimpse of the reality of the assumed impact of changing consumer purchasing behaviour. Among the major food service companies listed on the Singapore Exchange (SGX), Kimly Group, which operates a total of 136 multi-brand outlets with 84 coffee shops (as of October 2021), and JUMBO Seafood, which is famous for its seafood dishes, operates total 42 restaurants under 12 restaurant brands. Looking at the sales figures for the first half of the year (ending September) over the past three years, using the example of the JUMBO Group, which operates domestically and internationally, it is possible to understand the strong performance of the Kimly Group (Figure 5). Moreover, the JUMBO Group, which has mainly targeted tourists and business customers, has announced plans to acquire a 75% stake of the shop “國記雲吞麺” in the hawker centre for S$2.1 million (approximately JPY 200 million) in November 2020 under COVID-19 and to open multiple outlets both domestically and internationally. As of August 2022, “國記雲吞麺” has expanded to eight outlets, mainly in coffee shops in Singapore, and this is an excellent example of large food and beverage companies, which until now have mainly opened outlets in street shops and shopping malls, accelerating the opening of outlets in hawker centres and coffee shops based on changes in the business environment and consumers’ purchasing behaviour.

What measures can be taken to increase the profitability of coffee shops?

It is vital to implement measures without thinking outside the box.

Regardless of whether the investment is in a coffee shop or a shopping mall, there is a common need to increase the earning power of the tenants so the property owner can benefit from the rental income and future gains from the tenants. So what measures can coffee shops take to increase the profitability of their tenants, i.e., small-scale restaurants? The following are five ideas to consider.

The first is to optimise the tenant mix (the combination of restaurant types and business categories in which they open) and merchandise (the product range and pricing strategy offered by each restaurant) to maximise the number of customers and customer spend for the coffee shop as a whole, rather than for each individual restaurant. For example, a coffee shop owner regularly adds high-profile restaurant brands to his tenants to prevent existing customers from leaving and attract new customers at the same time. Another owner, who also manages several tenancies himself, attracts more customers to the coffee shop by offering lower-priced food at a lower price point, while another tenant, who offers higher-priced but comparable quality food to restaurants in the city, ensures that the coffee shop is profitable.

The second is to change not only the menu offered but even the signage of the shop in order to respond to the needs of the customers who visit the shop on different days of the week and at other times of the day, as well as the consumer profile of the area around the coffee shop. Even though the rent for the tenants of coffee shops is a fixed cost, many shops are only open for a limited number of hours, such as from morning to evening on weekdays. For example, coffee shops in office areas are surrounded by restaurants and bars that are busy after five on weekdays and cafés that are packed with cyclists, mainly Westerners, on weekend mornings; however, they are not open after the evening on weekdays or weekends. We believe that sales can be steadily increased by developing a menu such as smoothies that stick with the health-conscious attribute immediately after exercise on weekends, and alcohol and snacks in the evenings on weekdays.

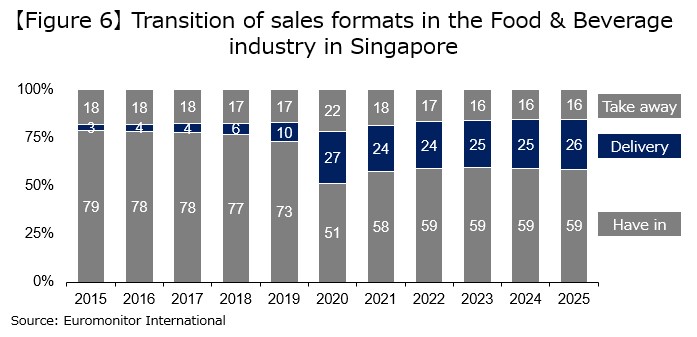

The third is to develop menus and stimulate potential demand, not only for in-store dining in coffee shops but also for takeaway and food delivery, in order to increase turnover and occupancy rates per tenant. While the small number of seats means a waiting time before being seated, there is high demand for takeaway food in coffee shops adjacent to offices and residences. In addition, food delivery, which has become more popular due to COVID-19, is expected to continue to be used on a daily basis as the new normal (Figure 6), and small-scale restaurants in coffee shops must develop their services in line with the changing purchasing behaviour of consumers.

The fourth is to focus on digital marketing activities using social media such as Facebook and Instagram. In particular, Generation Z, born between 1996 and 2015, are also known as “digital natives” as they were born in an age where digital is commonplace, and it is not uncommon for them to decide what to eat and where to eat based on information obtained from social media. Therefore, it is essential to develop menus that stick with Generation Z while simultaneously providing effective promotional information on social media, which they are in contact with at all hours of the day.

The fifth is to ensure thorough cleaning of the coffee shops, including tables, chairs and toilets as well. In order to prevent losing consumers who are unhappy with the cleanliness. Overall cleanliness of a coffee shop is an important factor that consumers subconsciously evaluate along with other factors such as the taste and price of food and beverages.

A need to fully understand the industry structure and consumers’ purchasing behaviour: Start with the daily use of coffee shops

Finally, we would like to discuss the business opportunities Japanese companies should know about coffee shops in Singapore.

Firstly, Japanese food and beverage companies should consider opening coffee shops as an option. We have an impression that most Japanese food and beverage (F&B) companies only consider opening new outlets in street shops and shopping malls in prime and downtown areas of Singapore. Many Japanese F&B companies are not even aware of the existence of coffee shops. However, as mentioned above, many Singaporeans spend more on eating out and takeaways in coffee shops, hawker centres, and food courts rather than in restaurants, cafés, and pubs. The ignorance of the importance and potential of coffee shops could be a risk and lead to lost opportunities. Whether or not they are aware of this consumer purchasing behaviour, some Japanese restaurants and cafés have recently become prominent in opening outlets in coffee shops; however, only a few have been expanding steadily. For example, Li Yuan Mee Pok, which has six outlets on the island, is gaining a growing presence as a popular restaurant in coffee shops across the country, offering “Japanese Fusion Mee Pok”, combining a local dish called mee pok, thick noodles similar to Japanese kishimen noodles, with a sour sauce and unique flavours such as miso and soy sauce, and toppings such as pork.

Furthermore, Japanese food companies seeking to develop sales channels along with the local authorities and banks supporting these companies should also consider coffee shops as a sales channel. Some Japanese food companies that engage in what they call ‘sales channel development’ activities in Singapore are often satisfied with the fact that their products are used in pilot or temporary events at only a few high-end restaurants or supermarkets and are not concerned about making money through permanent sales or increasing sales volumes. Although it depends on the type and price range of local products sold, the growing importance of merchandising in coffee shops and the fact that almost no Japanese products are sold in coffee shops, compared to the popularity of Japanese products in Singapore, make it difficult to differentiate Japanese food and beverages from other products on the menu.

It is strongly recommended that these Japanese companies, as well as local governments and banks, consider business opportunities based on an essential understanding of the structure of Singapore’s F&B industry and consumers’ purchasing behaviour from a frontline perspective, with a focus on coffee shops and hawker centres. The vast majority of Japanese people living in Singapore do not even use coffee shops, let alone know the difference between coffee shops and hawker centres. We would like to conclude this business consulting report by recommending that consumers start using coffee shops daily and understand through first-hand experience how easy they are to use and how essential they are to their daily lives.