Japanese corporations have been using cross-border M&A activities as an avenue to expand and acquire new markets, products and technologies. While ASEAN is an attractive investment destination, it requires appreciation of local knowledge to maneuver investments and operations in this region. This article explores some challenges that IGPI Singapore has observed in our experience, and hopes to create an awareness on the intricacy of cross-border collaborations.

Rise of Japan’s Outbound M&A Activity

Japan’s outbound M&A activity has risen sharply over the past years, driven by demographic and economic shifts, encouraging government initiatives and low funding cost.

As a shrinking population and lackluster domestic economic growth limit internal expansion potential, Japanese corporations are increasingly looking overseas for growth opportunities. Beyond that of tapping on existing capabilities to create new markets overseas, Japanese corporations can also acquire new products and technologies through cross-border M&A.

Prime Minister Shinzo Abe’s pro-global business policy has encouraged both inbound and outbound investment. Government organizations such as Japan External Trade Organization, Development Bank of Japan and Japan Bank for International Cooperation are instrumental in fostering a conducive environment for strategic overseas investments. This has brought about a mindset change of Japanese corporations to venture globally.

With a loose monetary policy aimed at stimulating economic growth, Japan’s low to negative interest rate encourages Japanese corporations to invest at a low funding cost. Coupled with cash reserve from operations and internal resources, Japanese companies are able to compete on price for attractive targets with their lower hurdle rate.

The Fundamentals of Overseas Expansion

Before any M&A activity, a corporation (Japanese or not) needs to first map its growth strategy. Once M&A has been identified as part of the growth strategy, a deal framework spanning the entire M&A spectrum should be established.

A strategic road map enables a corporation to plan and set action plans to achieve goals that are aligned to the vision. Top executives need to communicate a clear vision of the corporation to employees. Employees should be empowered to achieve stated goals and objectives with actionable strategies and plans. For instance, a corporation with a vision to be the leading technology firm globally could have goals of highest market share, driven by plans to hire top-notched employees and acquire leading technology firms globally.

Cross-border M&A requires careful planning and expertise to achieve the desired effect. Firstly, the strategic rationale for acquisition should be clear – whether it is for expansion of the core business in a new market, foraying into an adjacent business, or other purposes.

Secondly, suitable potential targets that fit the strategic rationale should be identified. Local advisors with local networks and market knowledge are helpful in searching for such targets. Corporations should also identify sources of synergies with the targets and quantify them at this stage.

Thirdly, structuring, due diligence and valuation should take place after a certainty of interest has been mutually established. Structuring should consider tax impact (corporate tax, capital gains tax, withholding etc.), regulatory regime and ease of profit repatriation. Common areas of due diligence include financial, tax and legal. Investors should also consider foreign direct investment restrictions that vary by countries and sectors and plan accordingly. Valuation helps form the basis for price negotiation, and aids in synergy quantification (if any).

Fourthly, post-merger integration should be planned and executed to achieve the intended effects. It is a folly to think that synergies will realize itself without concise effort. Planning for post-merger integration should start from the beginning of the deal, and include areas such as revised organization structure, reporting line, roles of employee, IT system integration. An in-house steering committee coupled with external change management experts will be helpful.

Finally yet importantly, M&A is a reiterative learning process that is honed through ongoing review of performance. Corporations that actively seeks growth through M&A should ideally have a dedicated M&A team that shares knowledge, and periodically compares the intended and actual outcome. It might make sense to exit from the investment at times.

ASEAN as An Investment Destination

Association of Southeast Asia Nations (“ASEAN”) is an emerging region made up of 10 distinct countries, with immense business potential from its booming population of over 650 million. With a combined gross domestic product of US$3.0 trillion in 2018, it is the third largest economy in Asia (behind China and Japan). ASEAN received US$1.5 trillion of foreign direct investment in 2018, topped by Singapore (50%), Indonesia (14%) and Vietnam (10%).

Vietnam has been gaining positive attention in recent years in light of the US-China tension, supportive government that is opening the borders and making doing business easier, fast growing and stable economy that created a rising middle-class population and a large population of over 97 million where 70% is under 35 years of age. IGPI has a Hanoi office that works closely with the local government on restructuring of state-owned enterprises.

With a geographical proximity to Japan, ASEAN is a popular investment destination for Japanese corporations. Especially for small and medium-sized deals (IGPI defines as less than US$500 million in enterprise value), ASEAN might be more popular than conventional investment destinations such as United States of America, Europe and China.

ASEAN has a wide range of opportunities such as being a low cost manufacturing base, housing a rising middle class population that represents a huge consumer market, and booming industries in infrastructure, digital economies, renewable energy, healthcare, education and others. Coupled with its open policy on international trade and dealings, it is little wonder that ASEAN has been gaining traction as an investment destination.

Challenges of Japanese outbound M&A

While Japanese corporations are renowned for their professionalism and knowledge, there are still challenges observed in cross-border M&A activities in ASEAN. Challenges observed are (1) lack of appreciation for the ASEAN’s diverse business-operating environment, (2) extensive information and reporting requirement, and (3) hierarchical structure with multiple layers of mid-management.

Lack of appreciation for ASEAN’s diverse business-operating environment

ASEAN is a diverse region with different languages and cultural backdrops, requiring sensitivity in the M&A process as well as post-merger integration. Maneuvering such differences require awareness and sensitivity, and a local advisor might be able to bridge the gap. For instance, certain ASEAN regions are straightforward and upfront with their opinions, while some Japanese might be reserved and indirect in their conversation. It is also common for CEO and/or founder of small-medium enterprises in ASEAN to attend meetings where decisions can be made, while mid-management of Japanese corporations who might not have decision making authority might attend such meetings.

In the case of post-merger integration, respect for local culture and working style is essential to motivating employees. For corporations who send Japanese managers to oversee the local operations, it is also important to build rapport with local managers to train talent and delegate authority accordingly. Change can only happen when the local managers and employees are empowered and engaged.

Extensive information and reporting requirement

As information, documentation and processes in ASEAN’s small-medium enterprises might not be as complete as Japanese corporations, due diligence might be a painful process for both parties. The target might have trouble gathering and preparing the due diligence request of the acquirer. Layers of approval required in some Japanese corporations also implies negotiation is a long drawn process, causing frustration and sometimes resulting in a no-deal. If the deal successfully closes, such reporting and governance structure might be difficult for local companies to adopt.

Hierarchical structure with multiple layers of mid-management

Big Japanese corporations typically have layers of hierarchy that might not be transparent to outsiders. Mid-management (such as in regional headquarters) might not have sufficient authority to make decisions, which might cause a longer process with confusion along the way. As the key performance indicator of the mid-management might not be aligned to the corporation, M&A might not be evaluated appropriately. For instance, measurement by number 4 of M&A activities might cause over-paying for the deal, while measurement by return on investment might lead to over-cautious evaluation and missing the deal. Targets (and acquired companies) might feel frustrated that the decision-makers do not hear what is said, and communication is merely a top-down approach.

Communication is a two-way street that can prevent unhappiness arising from differences. Begin with an understanding and appreciation of the differences, and communicate frequently to address feelings of parties. For instance, due diligence requirement and timeline can be communicated upfront so that the acquirer can prepare the target for the requirement, and the target can manage the expectation of the acquirer on the availability of such information. Skepticism of the acquired local companies on perceptions such as glass ceiling of foreign employees in a Japanese corporation and rigid working culture can be allayed through communication. Differences in another perspective, is a good way to grow as parties learn the positives from each other and create a mutually beneficial arrangement.

The world is your oyster (or sashimi)

Despite the divides that seem to be surfacing in today’s world, IGPI Singapore believes that the world will benefit with cross-border flow of information, people and capital. Being a firm that provides deal support from strategic planning to execution to post-merger integration, IGPI adds value through our local network and market knowledge. Corporations no longer look at just the domestic market in this interconnected world. Opportunities are yours to identify and pick, competitions are yours to navigate and overcome – are you ready for it?

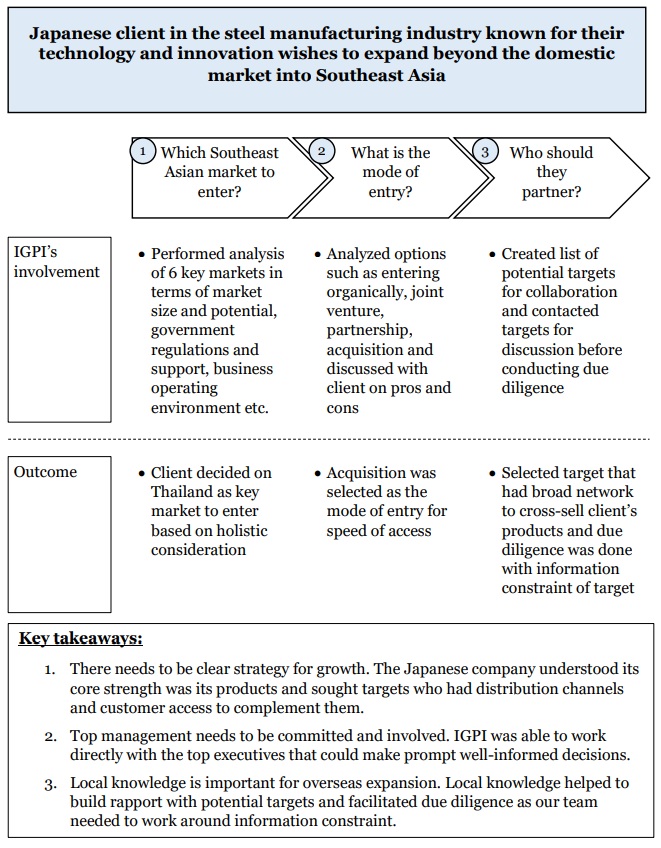

Case study:

IGPI’s overseas expansion support from strategic planning to M&A advisory