The Indonesian telecommunication sector has undergone a series of “evolutions” predominantly caused by digitalization, driven largely by increasing data consumption. This has triggered a set of “assets reorganization” activities marked by consolidations, mergers and acquisitions (M&A) and divestments and the creation of infra-co.

Some of these activities are propelled by capital markets that have seen an increase in activity in the infrastructure private investment and higher cost of funds. More importantly, however, central to these is the convergence of telecommunication services that has now been largely driven by data connectivity and the demand for high-speed, high-quality and affordable communication.

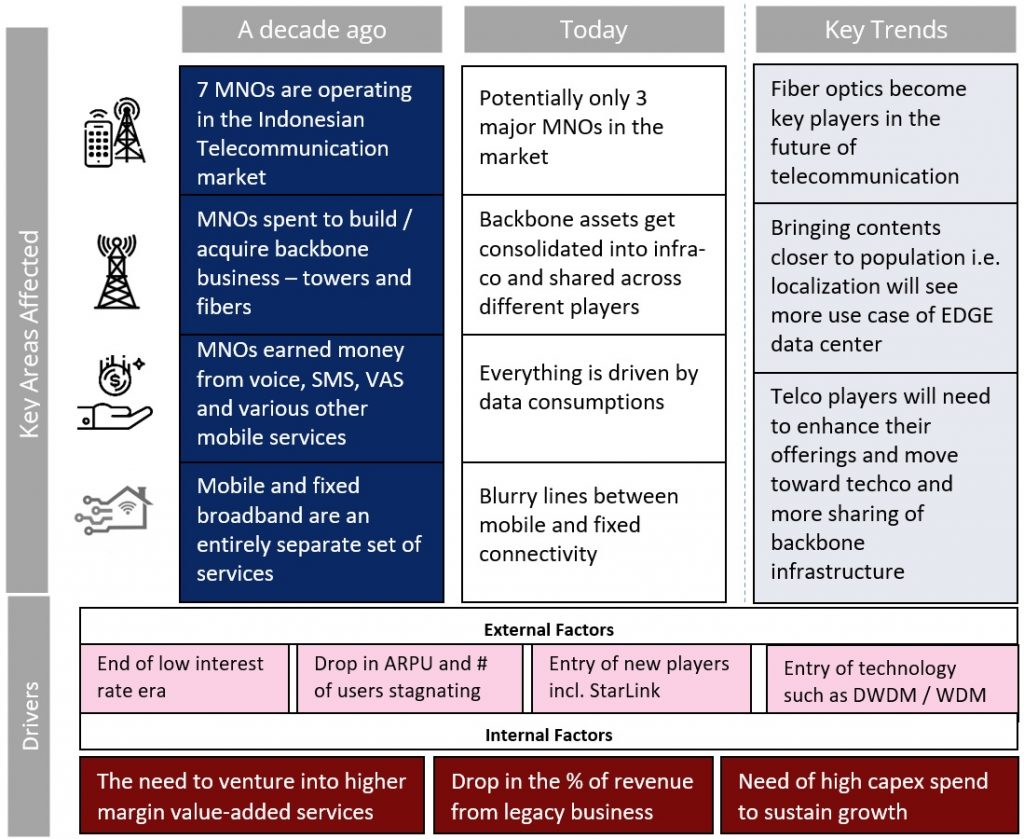

The Indonesian telecommunication sector has long been “mobile-centric,” primarily driven by mobile use as a more affordable and practical connectivity option. Before the wave of consolidation that occurred nearly a decade ago (sometime in 2015-16), there were 7 mobile network operators (MNOs) in Indonesia, namely Hutchison 3, XL Axiata, Indosat Ooredoo Hutchison, Sampoerna, Telkomsel, SmartFren and Bakrie Telecom.

Today, due to this wave of consolidation among these players (as detailed out in the table below) we are left with four key major MNOs. Soon, the country may only have three MNOs, as there is a potential merger between SmartFren and XL Axiata.

In addition to the wave of M&As among the MNOs, the Indonesian telecommunication sector has also witnessed a rise in divestments of telecommunication infrastructure assets, including telecommunication towers, data centers to fiber optics assets.

This trend it highlighted by the recent announced divestment Telkom Sigma, a subsidiary of Telkom Indonesia (a state-owned enterprise telecommunication company), and the proposed divestment of Indosat Ooredoo’s Fiber Optic and Marine Cable businesses.

This shift further underscores the ongoing reorganization of the Indonesian telecom sector.

Amidst these ongoing consolidations and divestments, we have also observed key emerging trends (discussed in further details below), including the rise of fixed-mobile convergence (FMC) in the Indonesian telecommunication landscape. This trend is exemplified by XL Axiata’s acquisition of Link Net, a major Indonesian fixed broadband player (initially owned by First Media, a subsidiary controlled by the Lippo Group and has been invested by a global PE, CVC), and the recent merger of Telkom’s subsidiaries – IndiHome (a fixed broadband service provider) and Telkomsel (one of the major MNO operators).

Underlying these corporate actions, is the significant increase in data consumption driven by digitalization and consumers’ contents consumption. This has made it strategically imperative for Indonesian telecommunication players to provide better quality and high-speed internet connections to grow their market share.

Specifically, in Indonesia, the fixed broadband communication segment has ample room to grow. The country currently has the lowest fixed-broadband penetration at less than 20%, significantly below Southeast Asia’s average of 40%, highlighting a significant opportunity for expansion and fiber optics investment in Indonesia. (DBS, 2023)

Furthermore, the services provided today are sub-standard, with average speeds that users typically get from the current fixed broadband internet service providers (ISPs) being only 31.42 Mbps, a far cry from the SEA internet speed of about 77.5 to 284.93 Mbps. (Ookla, Q2 2024)

This underscores the pressing need for improved broadband infrastructure and services in Indonesia, which could further drive the adoption of fixed-mobile convergence and accelerate 5G development to meet the growing demands of its digital population.

From our research and analysis, the bouts of divestment and M&As that happen in the Indonesian telecommunication market are mainly driven by several external and internal factors including but not limited to the following:

<External Factors>

1. The end of the low interest-rate era, bringing about an increase in the cost of funds, has raised the bar for return on invested capital.

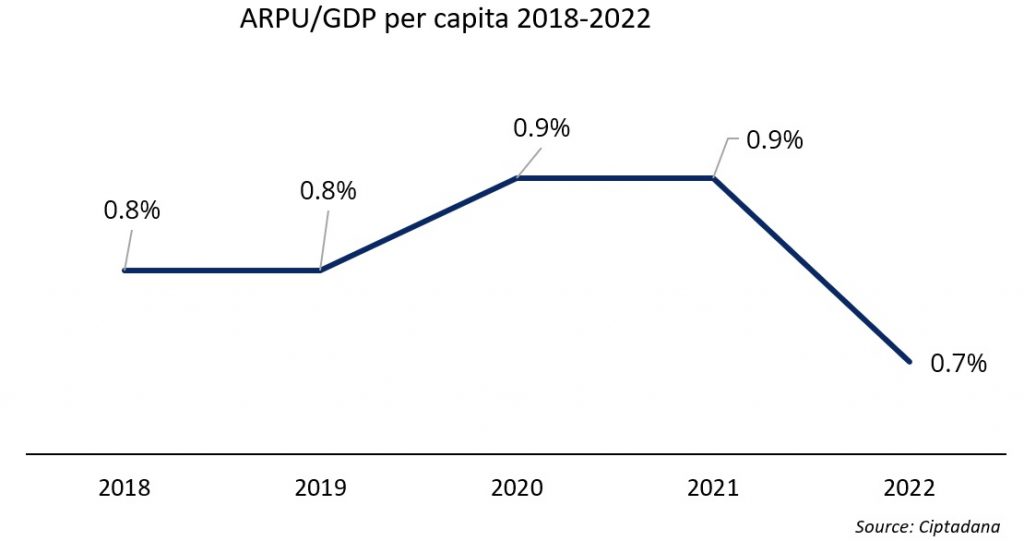

2. Heightened competition among the MNOs driving Average Rate per Users (ARPUs) downwards (shown by the decline in the ARPU/GDP Ratio in the chart below), while the number of subscribers remain stagnate.

3. Technological change, including the use of DWDM (Dense Wavelength Division Multiplexing) / WDM (Wavelength Division Multiplexing) which essentially allows for a single fiber optic to cater for various data signals use has expanded the bandwidth capacity of a single fiber optic, making fiber optic use capacity more efficient.

4. The entry of new players in the market, especially with the recent entry of Starlink (the satellite internet entity belonging to Elon Musk), has intensified competition in the Indonesian telecommunication sector. Starlink offers an alternative way for consumers to access the internet; adding pressure to the already competitive landscape, though its reach is currently limited.

<Internal Factors>

1. The need for MNO players to seek new avenues for growth including providing higher value-added services, has become increasingly important.

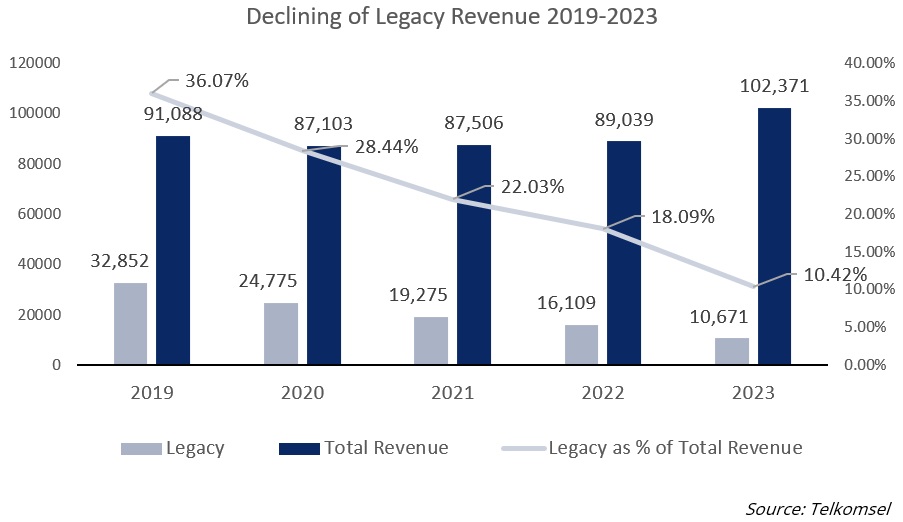

2. Adding to this is also the decline in legacy revenue streams (voice calls, SMS) for mobile companies, which now only provide a meager portion of the overall revenue (see below illustration on the proportion of legacy revenue to the total revenue of Telkomsel)

3. The high capital expenditure (capex) required to maintain competitiveness and/or to capture new markets has further driven the assets-reorganization. Combined with (1) and (2), this has triggered the slew of consolidation and divestment within the Indonesian telecommunication sector.

A confluence of these factors, coupled with the shift towards data-driven revenues, has resulted in the continuous shake up in the country’s telecommunications sector.

Driven by the rise of data consumptions and the strive for efficiency, the key trends in the telecommunication market in Indonesia will be mainly driven by the need to provide high quality communication more effectively i.e. higher quality and at lower price. Due to this reason, we likely to witness the key following trends:

1. Fiber optic investment in Indonesia will become crucial for the future of telecommunications, with FMC convergence and fiberization enabling high-quality, affordable internet

Driven by increasing need of data, fiber optic, with its ability to channel vast amounts of data efficiently and effectively and with its already proven technology, has been the clear winner. In addition, the use of DWDM and WDM technologies is a breakthrough that has increased the amount of bandwidth capacity that can be channeled by a single fiber optic network.

Adding to that, fiberization – which is basically connecting tower to the fiber optic cable becomes the key for 5G development in Indonesia. We have seen this done in major markets such as India and China. This also means there is a convergence whereby fixed broadband will generally empower the telecom tower. Hence Fiber optic is a clear winner of this transition and evolution.

2. EDGE Data Center will provide further content localization

With increased content consumption, placing content closer to users to reduce latency has become ever more important. Edge data centers (EDGE), which is essentially smaller sized data center closer to the population of end users and utilization of content delivery network (CDN), which is essentially network of servers with the goal of delivering content quickly, cheaply, reliably, and securely as possible, are crucial in this “localization” effort.

3. Telecommunication companies will evolve to become “techcos”, whereas infrastructure companies will focus on deepening their infrastructure play, creating a more scalable back-end sharing economy

With the creation of “infra-co” companies, separating infrastructure ownership from operations, is supported by the rise of infrastructure investors, particularly infrastructure private equity funds, seeking exposure to digital infrastructure.

Whilst operating-co will focus on providing more value-added, higher return and technological based servicing. We can already see this happening in developed markets such as Singapore, where Singtel and StarHub have made acquisitions in the enterprise services sector to expand their offerings in this area.

We in IGPI Singapore have been active in the telecommunication sector in the region, working with not only key telecommunication clients across various spectrums, but also with various infrastructure and non-infrastructure investors who are looking into investing and getting exposure into the SEA telecommunication market. We are happy to discuss and assist you on your strategy and investment matters.

To find out more about how IGPI can provide consulting support for businesses, browse through our insight articles or get in contact with us.

Mr. Erwin Thio is the Senior Manager of IGPI Singapore. His areas of expertise are in M&A deal management (both buy-side and sell-side), deal structuring, valuation and commercial due diligence, market analysis, and project management. He has also spent several years working within the investment and fund management (particularly for Real Estate Private Equity Funds) division of major developers such as Mapletree, Lendlease, Savills IM, and CFLD, where he helped with deal execution and origination, capital raising, fund creation/ development, and management.

Mr. Nicholas Quek is an Associate of IGPI Singapore. He graduated from Singapore Management University with a Bachelor of Business Management, majoring in Finance. During his time in university, he gained internship experience at OCBC bank where he took on a compliance role responsible for AML. He was also a Teaching Assistant for Financial Markets and Investments, and a Research Assistant for Real Estate Investment Trusts (REITs). In his final year, he embarked on an experiential learning course where he formulated strategies to increase e-commerce sales for an MNC.

Mr. Darren Hardisurjo is an Intern at IGPI Singapore (August 2024 – October 2024).

Industrial Growth Platform Inc. (IGPI) is a Japan-rooted premium management consulting & investment firm headquartered in Tokyo with offices in Osaka, Singapore, Hanoi, Shanghai & Melbourne. IGPI was established in 2007 by former members of Industrial Revitalization Corporation of Japan (IRCJ), a USD 100 billion sovereign wealth fund focusing on turnaround projects in Japan. IGPI has 13 institutional investors, including Nomura Holdings, SMBC, KDDI, Recruit & Sumitomo Corporation, to name a few. IGPI has vast experience supporting Fortune 500s, government. agencies, universities, SMEs, and funded startups across Asia and beyond for their strategic business needs and hands-on support across a wide variety of industries. IGPI group has approximately 7,500 employees on a consolidated basis.

* This material is intended merely for reference purposes based on our experience and is not intended to be comprehensive and does not constitute as advice. Information contained in this material has been obtained from sources believed to be reliable, but IGPI does not represent or warrant the quality, completeness and accuracy of such information. All rights reserved by IGPI.

Copyright© 2026 Industrial Growth Platform Pte. Ltd. All rights reserved. Web Excellence by Verz