Australia offers a very promising startup ecosystem with interesting innovation in a plethora of sectors. However, many Australian startups are faced with challenges of a small domestic market, lack of venture funding (especially early stage) and limited knowledge of international markets. These parameters are restricting promising Australian startups from achieving their true potential and scale. Finding apt strategic partners who can support with complementary knowledge, potential funding and established international market footprints can help such startups to blossom in and beyond Australia!

Right before the onset of the pandemic, Industrial Growth Platform Inc. (IGPI) established its Australian office in early 2020 in Melbourne. IGPI is a premier Japanese consulting and M&A advisory firm with offices in Japan, China, Singapore, Vietnam and Australia. One of the aspects that adds to our uniqueness is the fact that apart from providing strategic advice to Fortune 500s, Governments and startups, IGPI also makes principal investments (~40+ till date) and is associated with diverse array of investment initiatives in several countries. This includes investing in established transportation businesses, university-born startups, concession projects such as airports and VC with prominent LPs such as Honda and Panasonic. As a result, when IGPI was evaluating the Australian market, it was paramount to see it through diverse lenses which led to a number of candid in-country interactions (~150 meetings) before we finally decided to set shop.

One of the interesting things that we spotted during the meetings and innovation events was that the quality of innovation in Australia across sectors (e.g. agritech, cleantech, healthtech, fintech, spacetech etc.) is promising with a strong enthusiasm for building and scaling startups. However, wearing our Japan/Asia hats, we struggled to recall many names when it comes to Australian startups that ‘made it big’ internationally. The result was quite similar in other casual conversations that we had in professional circles in Singapore and Japan. This made us investigate this disconnect further.

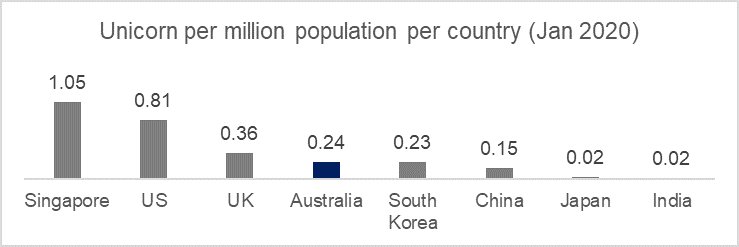

If the number of unicorns is considered any appropriate yardstick to measure a country’s startup ecosystem’s success, around 80% of the ~500 unicorns of the world (as of Oct 2020) hail from USA and China alone compared to a modest 6 from Australia, namely Afterpay, Airwallex, Canva, ZipMoney, Zoox and 10X Genomics1. Even if we compare the number of unicorns in proportion to their populations, Australia lags behind the likes of Singapore, USA and UK (see Figure 1). The burning question is: what is stopping Australian startups from making it big in the international scene?

Figure 1: Statista, World Bank

1.) Small home market size and notion of ‘far away’ makes the journey to achieve scale tougher

⇒ Australia is a developed country with a respectable GDP and economic track record over the past decades. However, its small and scattered population for this massive country (land size wise) makes for a humble ~0.3% of the global population2. As a result, there is a concrete ceiling on the scalability of the Australian startups for most industries if they only focus on domestic business. This coupled with Australia’s (distant) location to other major markets makes the journey of scaling a startup even longer as there is a notion of ‘far away’ associated with it (which also implies issues such as time zone differences). As per World Economic Forum’s Enabling Trade Report, Australia ranks 127 out of 136 countries in foreign market access rankings, based on aspects such as trade barriers and margin of preference in destination markets3. This gives some flavor of the challenges faced by conventional Australian businesses in general when it comes to accessing foreign markets and adds to the notion.

⇒ Even if one would argue for the selective lucrativeness of the Australian markets, e.g. startups in mining/METS that are targeting and catering to Australia’s mega-mines have potential to do fairly well domestically without having to rely much beyond the Australian borders, there is a growing focus away from resources and such startups should also look at building more use cases with their capabilities in mid to long term. And those new use cases may not have lucrative markets within Australia and will sooner or later also feel the need to internationalize to achieve their true potential. This view can have applicability to other startup areas too – after all we live in a globalized world! Therefore, apart from fueling growth, scaling up beyond Australian shores is always healthy from a risk diversification perspective too.

2.) Lack of funding pushes many startups into the valley of death

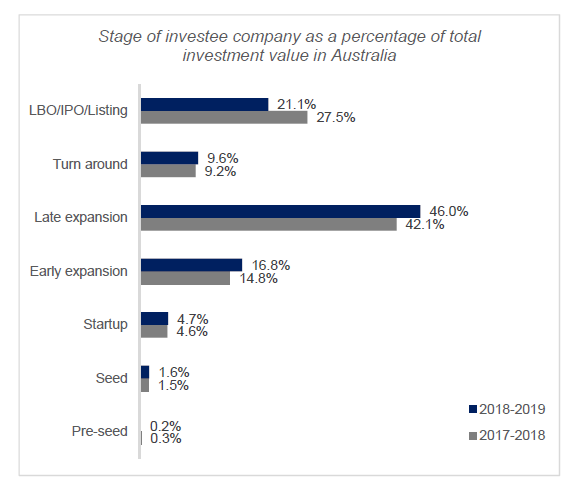

⇒ By developed world standards, Australia is considered quite risk averse4 as a country unlike its counterparts such as USA where startup culture is celebrated and VC investing is quite common (and fashionable) – especially early stages. The risk averse behavior can also been seen from the proportion of investment received by early stage companies as compared to more mature/established counter parts5 (see figure 2). As per a survey shared on StartupDaily, more than 70% of the VCs in Australia said that their average deal size in 2019 was in excess of A$ 1 million6 which reflects the graveness of the situation in especially in early stages. If we look at macro indicators, Australians are quite wealthy by global standards7 but probably the inherent conservatism has led them to make investments in more conventional asset classes such as real estate which has worked well for many in the past and that is possibly why angel / early stage funding is not as common as it ideally should be. Also, focusing on Government sources such as grants may not be the ideal answer to address this issue which primarily requires private participation and risk taking. This is the issue from the ‘supply side’ of early stage capital

Figure 2: Australia Bureau of Statistics

Figure 2: Australia Bureau of Statistics

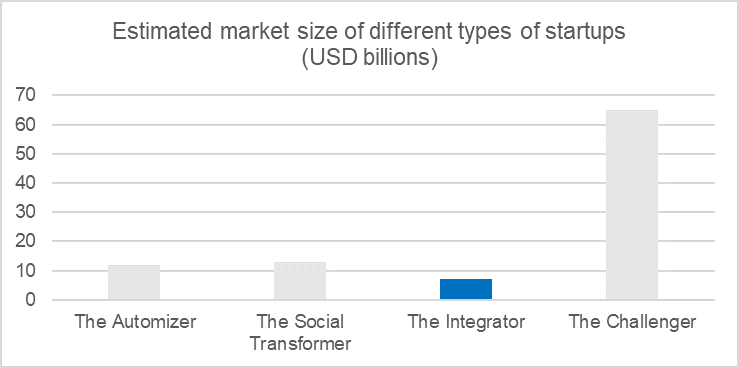

⇒ If we also evaluate this from the other side i.e. ‘demand side’ of the capital and look into the type of Australian startups and compare with the Silicon Valley, there is a higher percentage of “integrator” type startups8 (Integrator startups most frequently attack existing markets by providing a product that is cheaper than the alternatives) – which are usually considered “safer businesses” compared to the ones that challenge the status quo. Unfortunately, “integrator” type businesses have lower scalability than the “challengers” provided they ‘get it right’9 (see figure 3).

Figure 3: Testingsgblog

⇒ To corroborate the risk averseness further, as per a report titled Silicon Beach: A study of the Australian Startup Ecosystem, entrepreneurs in Silicon Valley explore new opportunities/markets 15% more frequently than Australian entrepreneurs, while entrepreneurs in New York seek new markets 12% more often8.

⇒ For both investors and investees alike, such factors impact the overall VC ecosystem and can especially dent early stage investing (later stage is relatively ‘safer’ since one can gauge the KPIs more realistically) which pushes startups in the valley of death and probably unknowingly killing the potential unicorns of tomorrow. At the end of the day, startup ecosystems run on a pyramid structure where the failure rate is surely high but if funding is not adequate, then the base of this pyramid will shrink (less startups) and hence lowering the chances of reaching the top of the pyramid i.e. scaled up success stories (irrespective whether a unicorn or not!).

3.) Limited knowledge / readiness for international markets results in selective internationalization

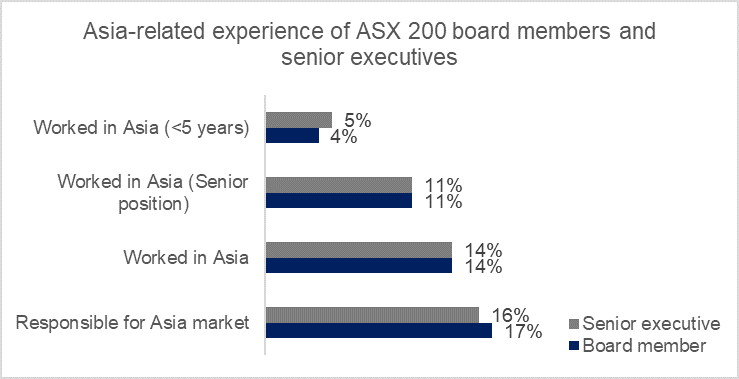

⇒ In our experience, some key factors that make startups successful are identifying the right issue(s) to solve, understanding the dynamics of the environment (3Cs), having a game plan (strategy; including internationalization) – and of course, a solid execution (apart from conventional aspects such as funding etc.)! In this competitive world, whether one is a B2B or B2C startup, internationalization and scaling seldom hurts anyone. In the larger scheme of this journey, building a startup and trialing/POCs in an Australian state can be compared to going to high school, expanding across Australia is like going to a university, and scaling internationally in complex (also less understood markets) outside one’s comfort zone is no less than attaining a PhD in that analogy! A general on-ground observation is that several startups aspire to go to USA and Europe (probably because of a comparable ease of doing business, notion of immediate market size and initial comfort etc.) and put other growing markets (as appropriate) on the back burner (e.g. Japan or ASEAN) which require more thought on aspects such as localization/product-market fit and also overcoming wider cultural barriers. But the journey can be worth the pain – whether through the lens of potential first mover advantage, risk diversification, geo-politics (at times) or with intent to uncover full market potential. For example, Japan continues to be one of the largest economy globally and ASEAN bloc is the 5th largest economy of the world10. Despite being a trading bloc (and a rapidly growing one), based on many on-ground conversations, Japan and ASEAN are not the first ‘port of consideration or entry’ on many startups’ lists. The common reason cited is lack of market understanding, language barriers and (perceived) market complexity of these markets! Generally speaking, even many listed Australian businesses and their leadership may not be ‘Asia ready’ but that may be where the next wave of opportunity lies for many11 (see figure 4)

Figure 4: AsiaLink Business

Using healthtech as an example, Australia is considered to be quite promising in this sector. Healthtech startups in Australia addressing issues relating to aging or infertility can evaluate potential markets based on commonality of issues and long term potential rather than just immediate attractiveness. For instance, several markets such as Japan could be potential markets as they face aging and fertility issues too12. Another example can be in the agritech space, where some problems being addressed by Australia’s agritech can have applicability to some ASEAN markets and we see prominent Japanese companies making investments in similar spaces in countries such as Vietnam13. There is scope for Australian startups to turn to those markets, attempt to localize and engage in the race either directly or via partnering locally (there can be many ways to penetrate a market and we strongly believe it can’t be a “cookie-cutter” approach especially in Asia).

It will be a battle half won if we only identify the key concerns of Australian startups that can keep them away from achieving their true potential and not find ways to address it. At the end of the day, successful scale up of any business depends on three aspects: (1) Information, (2) Know-how and (3) Execution.

How fantastic would it be if someone can support Australian startups with all the three aspects and in-turn aiding the three issues identified i.e. small local market, funding woes and lack of holistic knowledge related to geographic expansion?

The answer lies in finding a good strategic partner i.e. someone who brings you “more than just money” on the table – easier said than done but it can really prove to be beneficial. To complement this, many large Japanese companies are increasingly looking at building new businesses, digital transformation opportunities etc. and are welcoming startups that have differentiated offerings to collectively use the Japanese company’s wide Asia footprint, local knowledge and ability to invest along with the startup’s intellectual property for mutually beneficial long term value creation.

IGPI is well networked with most Japanese mega corporations and SMEs across Asia – be it Japan (HQ), ASEAN (RHQ in many cases) and Oceania offices and support them for a number of initiatives. If you are an Australian startup, we can assist you find the right potential partner for your market expansion plans beyond Australia.

IGPI provides highly customized Asia business advisory to its diverse range of clients including but not limited to:

Mr. Rachit Khosla is the Country Manager of IGPI Australia. Rachit is a seasoned strategy consulting professional with rich experience of leading and executing market entry and growth strategy (both organic and inorganic) engagements for Fortune 500 businesses and large MNCs across Asia. Rachit has advised clients in a diverse range of industries including automotive, fin-tech, manufacturing, med-tech & healthcare, construction materials, travel, IT & telecom. Before joining IGPI, his experience includes country manager at YCP Solidiance Asia Pacific and head of an online B2B bidding platform for the consulting industry.

Mr. Hui Fu Chua is an Analyst in IGPI Singapore. Hui Fu started his career with IGPI, where he performs research and data analysis to support the team in strategic planning and decision making. In IGPI, Hui Fu has been involved in assignments across different sectors such as renewables, mining, agriculture, healthcare amongst many others with a strong focus in the Australia, Japan and Southeast Asia markets.

Ms. Shrutee Chitre is an Intern at IGPI Australia (Aug-Oct 2020). Shrutee is currently pursuing Master’s in Management from the Melbourne Business School. She has had previous work experience of 5 years with Reliance Life Sciences Pvt. Ltd., a group company of an Indian MNC Conglomerate – Reliance Industries in Mumbai, India.

![]()

Industrial Growth Platform Inc. (IGPI) is a premier Japanese business consulting firm with presence and coverage across Asian markets. IGPI was established by former members of Industrial Revitalization Corporation of Japan (IRCJ) in 2007. IRCJ, a US $100 billion Japanese sovereign wealth fund, is known as one of the most successful turn-around fund supported by the Japanese government.

In 2017, IGPI collaborated with Japan Bank for International Cooperation (JBIC) to form JBIC IG, providing investment advisory services and supporting overseas investment. In 2019, JBIC along with BaltCap has jointly established Nordic Ninja, a €100 million venture capital fund to focus on deep tech sectors such as autonomous mobility, digital health, AR/VR/MR, artificial intelligence, robotics and IoT in the Nordic and Baltic region. In 2019, IGPI established IGPI Technology to focus in the area of science and technology. The company invests in technological ventures and provides hands-on management support. The company also provides business development support towards commercialization and monetization of technologies

IGPI Australia is a branch office of IGPI Singapore. The later which was established in 2013 focusing on management consulting and M&A advisory in Southeast Asia across various sectors. We act as a bridge between Japan and Southeast Asia, having advised on market entry strategy, potential target search, valuation, due diligence, M&A process management, post-merger integration and change management for leading Japanese clients. In addition, we have helped businesses in Southeast Asia enter Japan and acted as sell-side advisor for SMEs and private equity fund looking to divest. IGPI Australia was established in 2020 with a dual focus of helping Australian businesses enter and grow in ASEAN/Japan and attracting Japanese investments into Australia.

Get in touch with us on internationalization, strategic planning and M&A related topics!

IGPI Australia – contacts:

Kohki Sakata

Chief Executive Officer

+65 81682503

k.sakata@igpi.co.jp

Rachit Khosla

Country Manager – Australia

+61 414 433 572

r.khosla@igpi.co.jp

This material is intended merely for reference purposes based on our experience and is not intended to be comprehensive and does not constitute investment, legal or tax advice. This should not be regarded as an offer to sell or as a solicitation of an offer to buy any financial product, an official confirmation of any transaction, or as an official statement of IGPI. Information contained in this material has been obtained from sources believed to be reliable, but IGPI does not represent or warrant the quality, completeness and accuracy of such information. All rights reserved by IGPI.

Other sources such as but not limited to Statisa, World Bank, Investopedia were also referred to.

Copyright© 2026 Industrial Growth Platform Pte. Ltd. All rights reserved. Web Excellence by Verz